Every year, businesses that fail to remit sales tax cost state governments billions of dollars. That is exactly why many states require a sales and use tax bond before they will even let you open your doors — and if you skip it, your license could be denied, revoked, or never issued in the first place.

If your state is asking for one and you have no idea what it means, what it costs, or how to get it fast, this guide covers everything you need to know.

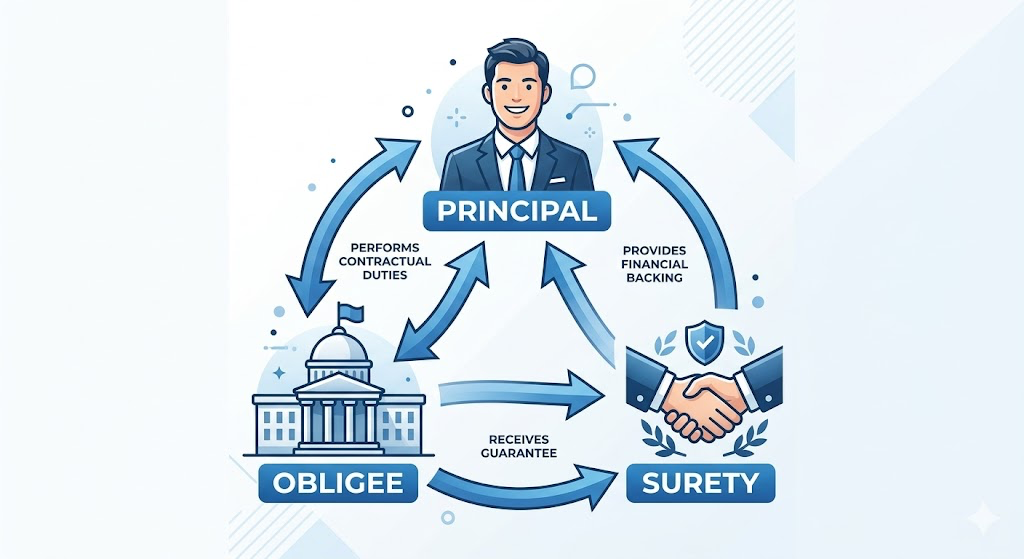

What Is a Sales and Use Tax Bond?

A sales and use tax bond — also called a sales tax bond, a continuous bond of seller, or a financial guarantee bond — is a type of surety bond required by state and local governments that guarantees a business will collect, report, and remit all applicable sales taxes on time.

It is not insurance for your business. It is a financial promise made to the government. If you fail to pay your taxes, the government can file a claim against the bond and recover those funds. The surety company pays the claim first — but then comes back to collect every dollar from you.

The bond is a three-party agreement:

| Party | Role |

|---|---|

| Principal | The business owner who purchases the bond |

| Obligee | The government agency requiring the bond |

| Surety | The insurance company that issues and backs the bond |

Think of the surety as a co-signer. They are putting their reputation and money on the line for you — but if things go wrong, you are ultimately responsible for repayment.

Who Needs a Sales and Use Tax Bond?

Not every business is required to post one upfront. In many states, the bond is triggered by specific conditions rather than being automatically required at registration. The most common situations include:

| Trigger | Details |

|---|---|

| New business in certain industries | Especially alcohol, tobacco, fuel, and marijuana |

| Prior tax delinquencies | Most states require bonds after repeated late filings or missed payments |

| History of returned checks for tax payments | Signals financial risk to the agency |

| Revoked license reinstatement | Required to prove financial accountability before reopening |

| Out-of-state vendors | Some states require bonds from remote sellers with use tax obligations |

States like Iowa set specific delinquency thresholds — quarterly filers who miss two payments within 24 months may be required to post a bond. North Dakota holds compliance bonds for five years, though businesses with two consecutive years of clean filings can request an early release.

The industries most commonly required to bond before operations even begin include retailers of alcohol, tobacco, fuel, fireworks, and cannabis products. General merchandise retailers may also need one depending on the state.

How Much Does a Sales and Use Tax Bond Cost?

The cost of the bond itself — called the bond amount or penal sum — is set by the government agency. It is typically calculated as a multiple of your average monthly or quarterly tax liability. Missouri, for example, sets bond amounts at three times the applicant’s average monthly liability. Iowa calculates it based on filing frequency:

| Filing Frequency | Bond Amount Formula |

|---|---|

| Quarterly filers | Equal to 3 quarters of sales tax liability |

| Monthly filers | Equal to 5 months of sales tax liability |

| Semimonthly filers | Equal to 3 months of sales tax liability |

| Annual filers | Equal to 1 full year of liability (minimum $100) |

Common bond amounts in the market range from $2,000 to $50,000, though they can go higher for larger businesses or higher-risk industries.

What you actually pay to a surety company is a premium — a small percentage of the total bond amount. For most applicants with good credit, premiums run between 1% and 5% of the bond. That means a $10,000 bond might cost you as little as $100 to $500 per year.

Businesses with lower credit scores will pay higher premiums — sometimes up to 10% — because they represent greater financial risk to the surety. However, bad credit does not disqualify you. Most surety agencies offer programs specifically for hard-to-place applicants, though you may need to provide additional collateral or financial documentation.

What Affects Your Premium Rate?

| Factor | How It Impacts Cost |

|---|---|

| Credit score | Higher score = lower premium |

| Business financial history | Clean books lower perceived risk |

| Bond amount required | Larger bond = higher total premium dollars |

| Industry type | High-risk industries (fuel, alcohol) may carry higher base rates |

| State requirements | Some states set minimum thresholds that drive costs up |

How to Get Your Sales and Use Tax Bond

Getting bonded is simpler than most business owners expect. The process typically takes less than 24 hours for straightforward applications.

Start by applying with a licensed surety provider — Swiftbonds works with businesses across all 50 states and can match you with the right carrier for your state and industry. Once your application is submitted, you receive a quote based on your credit profile and the required bond amount. After you pay the premium, the surety issues the bond documents — either digitally or as a physical document set — and you file it with the obligee (the state or local agency that required it). That filing is what officially satisfies the requirement and keeps your license in good standing.

Swiftbonds LLC

2025 Surety Bond Technology Provider of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

How Bond Claims Work

If your business fails to remit sales taxes as required, the obligee — the government tax agency — can file a claim against your bond. Here is what that process looks like:

The agency submits the claim to the surety company. The surety investigates to confirm the claim is valid. If it is, the surety pays the obligee up to the full bond amount. Then the surety turns around and demands full reimbursement from you — the principal.

A concrete example: you have a $10,000 bond and fall $7,000 behind on sales tax. The surety pays the state $7,000 to resolve the claim. You now owe the surety $7,000, plus potential legal and collection costs. The bond does not absorb the loss — it only guarantees the government gets paid first.

This is why the bond functions as a compliance tool, not a safety net for the business. Avoiding claims entirely is the goal, and it is achieved simply by filing and paying your taxes on time.

Bond Renewal: What Happens After Year One

Most sales and use tax bonds are issued for a 12-month term. Before the expiration date, the surety company will send renewal reminders and re-evaluate your credit standing. If your credit has improved since the original application, your premium may go down. If your credit has declined or a claim was filed, expect a higher rate.

If you allow the bond to lapse — even for a day — the government agency may consider your license suspended or revoked. Reinstatement usually requires a new bond application and potentially a higher bond amount if your tax compliance record has deteriorated. Do not let it expire without renewing.

Types of Sales and Use Tax Bonds

While “sales and use tax bond” is the umbrella term, the specific bond required depends on your industry and state. The most common variants include:

| Bond Type | Who Needs It |

|---|---|

| General Sales Tax Bond | Retailers of taxable goods in most states |

| Cigarette and Tobacco Tax Bond | Tobacco distributors, wholesalers, and retailers |

| Alcohol / Liquor Tax Bond | Brewers, importers, wholesalers, and retailers |

| Fuel / Motor Fuel Tax Bond | Fuel distributors, suppliers, and special fuel dealers |

| Cannabis / Marijuana Tax Bond | Dispensaries and producers in legal-market states |

| Customs Tax Bond | Importers and brokers dealing with taxable goods |

Some businesses may require multiple bonds across categories — for example, a retailer that sells both tobacco and fuel would likely need separate bonds for each product type depending on the state.

Corporate Officer Bond: A Lesser-Known Option

In some states — including North Dakota — a corporation, LLC, or limited liability partnership can post a corporate officer bond instead of having individual officers personally liable for unpaid tax obligations. This bond protects the officers themselves from personal financial exposure during tax periods when the bond is active. It is a strategy worth exploring if your business is a multi-member entity with significant tax liability.

What If the Bond Is Not Required Yet?

Not every business needs to post a bond at startup. In many states, first-time applicants with no prior tax issues begin operations without one. The bond requirement kicks in only if the agency identifies a risk factor — delinquency, returned payments, or a prior problematic tax history.

That said, some states (Missouri is a clear example) require all new retail sales tax license applicants to post a bond before the license is issued, based on projected or prior-owner liability. Always verify your specific state’s requirements before assuming you are exempt.

FAQs

Does having bad credit mean I cannot get bonded? No. While bad credit raises your premium, most surety providers — including those working with Swiftbonds — offer programs specifically designed for applicants with low scores or past financial difficulties. You may need to provide financial statements or additional collateral, but you can still get bonded and legally operate.

Can I get my bond refunded after a period of good compliance? Yes, in many states. Iowa refunds bonds after two years of satisfactory filing and payment. Missouri releases the bond after two years of clean compliance. North Dakota holds compliance bonds for five years but allows early review after two years. Each state has its own rules — check with your tax agency or surety provider.

What bond types does my state accept? Most states accept surety bonds, cash bonds, certificates of deposit, and irrevocable letters of credit. Personal checks are almost universally not accepted. Surety bonds are by far the most common and convenient option because they require no large upfront cash deposit.

How long does it take to get a sales and use tax bond? Most applications are processed within 24 hours. Overnight shipping is available for physical documents, and digital filing is accepted in many states.

What happens if I sell my business? The new owner typically cannot use your bond. They must apply for their own bond based on the prior owner’s tax history — which is often used to calculate the required bond amount. If the previous owner had a good record, this can work in the buyer’s favor.

Is a sales and use tax bond the same as sales tax insurance? No. They are structurally different. Insurance protects the policyholder. A surety bond protects the obligee (the government) — and the business owner is still ultimately responsible for any losses.

Conclusion

A sales and use tax bond is one of those business requirements that can feel overwhelming until you understand how straightforward it actually is. The government requires it to protect tax revenue. You purchase it through a surety provider, pay a small annual premium, and maintain it in good standing by simply doing what you are already required to do — file and pay your taxes on time.

Whether you are a first-time retailer navigating a state’s bonding requirement or a business owner rebuilding after a tax compliance issue, the bond is obtainable, affordable, and often issued within a single business day.

5 Interesting Things About Sales and Use Tax Bonds You Won’t Find in Most Guides

- The bond requirement predates the business opening in some states. Missouri requires a bond before the Department of Revenue will even issue a retail sales tax license — meaning a business that skips this step cannot legally make its first sale.

- The bond amount can be as low as $25. Missouri sets a minimum bond of just $25 for new businesses whose projected three-month liability falls under $500 — making it one of the most affordable compliance tools in the regulatory landscape.

- Your bond can protect corporate officers from personal liability. In North Dakota and similar states, a corporate officer bond shields the company’s managers and partners from being personally sued for unpaid sales tax during the period the bond is active — a protection that goes well beyond simple licensing compliance.

- A bond can be seized while you are still in business. If a taxpayer becomes delinquent, the state tax agency can redeem a certificate of deposit or cash bond immediately — without waiting for a court order — leaving the business scrambling to post replacement collateral within 30 days or risk losing the license entirely.

- The penny’s end affects how sales tax bonds are calculated. Since the U.S. Mint ended penny production in June 2025, states like Iowa and Nevada have issued guidance clarifying that while retailers may round cash transactions to the nearest nickel, sales tax must still be calculated on the exact gross receipts — meaning even this small rounding change has no effect on the tax liability that underlies your bond requirement.

Leave a Reply