Most business owners who offer a 401(k) or retirement plan to their employees have never heard of the ERISA bond — until a Department of Labor auditor asks for it. And when that happens, not having one is not just a paperwork problem. It is a federal violation that can trigger DOL sanctions, penalties, and the kind of scrutiny no employer wants.

If you manage or sponsor an employee benefit plan and nobody has told you about this requirement yet, this guide is written for you.

What Is an ERISA Bond?

An ERISA bond — formally called an ERISA fidelity bond — is a type of insurance coverage mandated by Section 412 of the Employee Retirement Income Security Act of 1974. It protects the employee benefit plan itself against financial losses caused by fraud or dishonesty committed by the people who handle plan funds.

The law is direct: “Every fiduciary of an employee benefit plan and every person who handles funds or other property of such a plan shall be bonded.”

The bond is designed to reimburse the plan — not to protect the individuals who manage it — if someone steals, embezzles, forges, misappropriates, or otherwise dishonestly takes assets from the plan. It covers acts including larceny, theft, forgery, wrongful abstraction, wrongful conversion, and willful misapplication.

One critical distinction is that this bond has no deductible. Coverage begins from the very first dollar of a valid loss, up to the full bond amount. That is a legal requirement, not a product feature.

ERISA Bond vs. Fiduciary Liability Insurance: Not the Same Thing

This is the most common source of confusion among plan sponsors, and it is worth addressing directly.

| Coverage Type | What It Protects | Required by Law? |

|---|---|---|

| ERISA Fidelity Bond | The plan’s assets — against theft and dishonest acts | Yes, under ERISA Section 412 |

| Fiduciary Liability Insurance | The fiduciaries — against claims of mismanagement or breach of duty | No, but strongly recommended |

| D&O Insurance | Directors and officers — against claims of negligence | No |

An ERISA bond covers crime. Fiduciary liability insurance covers mistakes. Your D&O policy almost certainly does not satisfy the ERISA bond requirement — and even if it includes a general fidelity provision, D&O policies typically carry a deductible, which ERISA forbids for fidelity coverage. Review every policy before assuming you are compliant.

Who Must Be Bonded?

Anyone who “handles funds or other property” of the plan is required to be covered, unless they qualify for a specific exemption. The DOL defines handling broadly. It is not limited to people who physically touch money. A person is considered to be handling funds if their duties or activities could cause a loss due to fraud or dishonesty, whether acting alone or in collusion with others.

The six criteria for determining whether someone handles plan funds:

- Physical contact with cash, checks, or similar property

- Power to transfer funds from the plan to oneself or a third party

- Power to negotiate plan property (mortgages, land titles, securities)

- Disbursement authority or authority to direct disbursement

- Authority to sign checks or other negotiable instruments

- Supervisory or decision-making responsibility over bonding-required activities

This typically includes the plan administrator, plan trustees, and any officers or employees of the plan sponsor whose duties involve receipt, safekeeping, or disbursement of plan funds. It can also extend to third-party service providers — such as a third-party administrator or investment advisor — if their employees handle plan assets directly.

Which Plans Are Exempt?

Not every plan requires a bond. The ERISA bonding requirement does not apply to:

| Exempt Plan Type | Reason |

|---|---|

| Completely unfunded plans | Benefits paid directly from employer’s or union’s general assets, not segregated |

| Governmental plans | Not subject to Title I of ERISA |

| Church plans | Not subject to Title I of ERISA |

| Solo 401(k) / owner-only plans | No employees covered, not subject to Title I |

| Certain regulated financial institutions | Banks, insurance companies, registered broker-dealers meeting specific exemption conditions |

A plan is generally considered funded — and therefore subject to bonding if funds are handled — if it has a trust or separate bank account, if employee contributions are segregated, or if it is linked to a Section 125 cafeteria plan that does not meet the specific safe harbor under DOL Technical Release 92-01.

How Much Coverage Is Required?

The bond amount is calculated based on the funds each person handles, not the total plan value.

| Scenario | Required Bond Amount |

|---|---|

| Standard plans | 10% of funds handled in the preceding plan year |

| Minimum bond | $1,000 per plan |

| Maximum bond (most plans) | $500,000 per plan |

| Plans holding employer securities (ESOPs, KSOPs) | Up to $1,000,000 per plan |

A concrete example: if a company’s 401(k) plan holds $1,000,000 and three employees — the trustee, the named fiduciary, and the plan administrator — each have full access to and transfer authority over those funds, then each person must be bonded for at least $100,000 (10% of $1,000,000).

If a single bond covers multiple plans, or a person handles funds for more than one plan, the bond may need to exceed the $500,000 cap to satisfy the 10% rule for each plan.

Qualifying vs. Non-Qualifying Assets: A Distinction Most Plans Miss

This is the aspect of ERISA bonding that catches the most plan sponsors off guard. The DOL draws a line between qualifying and non-qualifying plan assets, and it directly affects your required bond amount.

Qualifying assets are those held by regulated entities — banks, credit unions, insurance companies, or registered broker-dealers — and include mutual fund shares, annuity contracts, participant-directed accounts, qualified employer securities, and participant loans. These carry standard protections and are treated as lower risk.

Non-qualifying assets are investments without a readily determined market value and not available for standard public trading. Examples include limited partnerships, third-party notes, real estate, and collectibles.

If more than 5% of your plan assets are non-qualifying, the bond amount jumps significantly — to the greater of 10% of total plan assets or 100% of the non-qualifying asset total. There is an alternative: attach an audited financial report to your Form 5500 in lieu of maintaining the higher bond. However, that audit typically costs 10 to 20 times more than the bond premium itself. The bond is almost always the smarter financial choice.

What About Cybersecurity?

The DOL issued guidance in 2021 emphasizing cybersecurity risks to retirement plans and the fiduciary obligations they create. A cybersecurity incident — such as fraudulent wire transfers or unauthorized access to plan accounts — can rapidly become a fiduciary breach under ERISA.

Standard ERISA fidelity bonds may or may not cover losses from cyber-related fraud. The policy language varies by provider, and you should not assume cyber coverage exists without reviewing the terms explicitly. Some providers offer combination policies that bundle ERISA fidelity coverage with cybersecurity protection, which can be a smart option for plans with high digital exposure. Any such combination policy must still meet all other ERISA bonding requirements to count toward compliance.

The Form 5500 Connection

If your plan is large enough to file a Form 5500 with the IRS and DOL, you should know that Form 5500 directly asks whether the plan has a fidelity bond — and that form is signed under penalty of perjury. Answering incorrectly, or discovering during an audit that the bond was missing or inadequate, puts the plan sponsor in a difficult position. The DOL has the authority to assess substantial penalties against employers whose plans do not meet bonding requirements.

How to Get Your ERISA Bond

The process is straightforward, and for most plans it can be completed within a single business day. Start by calculating the correct bond amount based on the funds handled and the type of assets in your plan. Then apply with a licensed surety provider — Swiftbonds works with plan sponsors across all 50 states and can match you with a Treasury-approved surety quickly. Once your application is submitted, you receive a quote based on your plan details and number of individuals requiring coverage. After you pay the premium, the bond is issued and you keep it with your plan records. For bonds under $500,000, same-day issuance is often available.

Bonds must be obtained from a surety or reinsurer listed on the Department of the Treasury’s Listing of Approved Sureties (Circular 570). Neither the plan nor any interested party may have a financial interest in the surety, agent, or broker through which the bond is obtained.

Swiftbonds LLC

2025 Surety Bond Agency of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

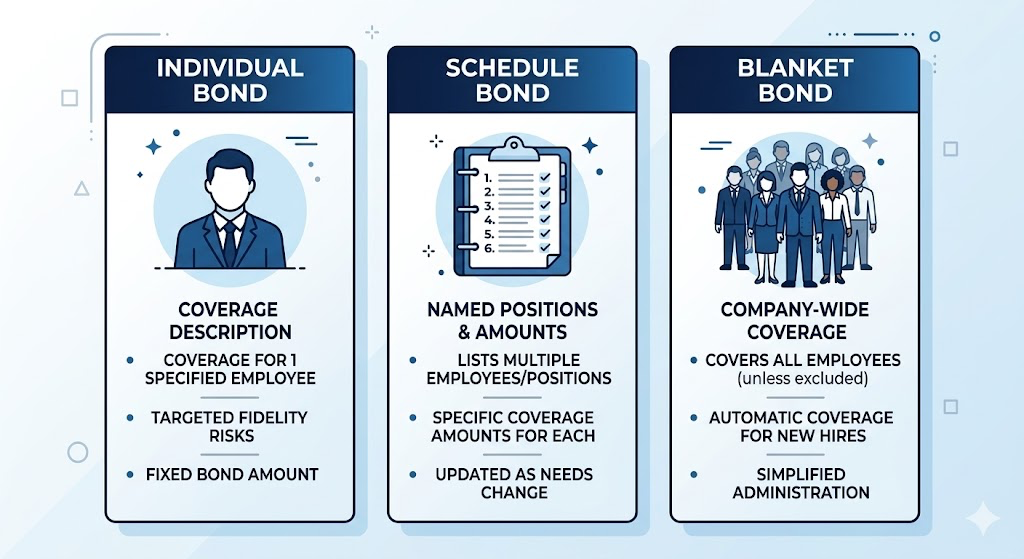

Individual, Schedule, and Blanket Bonds

Depending on your plan’s structure, you have three bond format options. An individual bond covers a single named person. A schedule bond covers a list of named individuals or specific positions. A blanket bond covers all individuals in roles that require bonding, without naming each one specifically. For most small and mid-sized plans, a blanket bond offers the most practical and cost-effective approach because it eliminates the need to update the bond each time personnel changes.

Multi-Year Bonds and Retroactive Coverage

ERISA bonds are typically issued for one-year terms, though multi-year bonds (two or three years) are available and often lock in the premium rate for the full term — providing both cost savings and administrative convenience.

On retroactive coverage: plan audits sometimes reveal that a plan has operated without a bond for prior years. Retroactive bonds are generally unavailable because most states prohibit insurers from issuing them. If this situation arises, the recommended approach is to document your compliance efforts going forward and work with the DOL to demonstrate remediation. Some providers offer retroactive coverage as a product feature — confirm whether it is available and what conditions apply before relying on it.

What Does the Premium Actually Cost?

No top-ranked competitor in this space provides premium cost ranges, so here is a practical reference. ERISA fidelity bond premiums are generally very affordable — often the least expensive compliance cost a plan sponsor faces. For a small to mid-sized plan with qualifying assets and straightforward fiduciary structure, a one-year premium for a $10,000 bond may cost as little as $100 to $200. Larger bond amounts and plans with non-qualifying assets will carry higher premiums, and the number of individuals or positions being covered can also affect pricing. Unlike many insurance products, credit score plays a smaller role in ERISA bond underwriting compared to the plan’s asset composition and structure.

FAQs

Does my solo 401(k) need an ERISA bond? No. Owner-only plans — also called solo 401(k) plans — are not subject to Title I of ERISA and are therefore exempt from the fidelity bonding requirement. The requirement applies only to plans covering at least one non-owner employee.

Can plan assets pay for the bond? Yes. The DOL explicitly permits plan assets to be used to purchase the ERISA fidelity bond because the bond’s purpose is to protect the plan. There is no conflict of interest in this arrangement.

Does our health and welfare plan need a bond? Possibly. Funded health and welfare plans — those with a trust, a separate bank account, or employee payroll contributions — are generally subject to ERISA bonding requirements. Completely unfunded plans where benefits are paid directly from employer general assets are exempt. The funded vs. unfunded determination requires careful review of how the plan holds and processes funds.

What happens if we don’t have a bond? Operating a plan without a required ERISA bond is an unlawful act under federal law. The DOL can assess substantial monetary penalties, and a missing bond discovered during an audit creates significant compliance liability for the plan sponsor and any fiduciaries who authorized plan handling without coverage in place.

Can a third-party administrator be bonded separately? Yes. A service provider can purchase its own separate bond insuring the plan, rather than being added to the plan’s existing bond. The plan sponsor may agree that the service provider will pay for that coverage, or the plan sponsor may add the service provider to the plan’s own bond. Either approach satisfies ERISA’s requirements as long as the coverage amount is adequate.

How often does the bond need to be updated? At the start of each plan year, you should recalculate the required bond amount based on the funds handled in the prior year. If the plan has grown significantly, the existing bond may no longer meet the 10% minimum and will need to be increased at renewal.

Conclusion

The ERISA bond is one of the few truly non-negotiable compliance requirements in the employee benefits world. It does not cost much, it is not complicated to obtain, and it provides a critical financial backstop that protects your employees’ retirement assets from the rare but devastating scenario of internal fraud or theft. Yet a surprising number of plan sponsors are either unaware they need it or are operating with a bond that no longer meets the required coverage amount.

Reviewing your bond annually — alongside your plan’s asset values and personnel changes — is a simple practice that keeps your plan in compliance and your employees’ benefits protected.

5 Interesting Things About ERISA Bonds You Won’t Find in Most Guides

- The ERISA bonding requirement predates the internet, smartphones, and email — but it now explicitly extends to digital fraud. The DOL’s 2021 cybersecurity guidance confirmed that unauthorized electronic access to plan accounts falls within the scope of fiduciary responsibility, and plan sponsors who ignore cyber risks may find themselves facing a fiduciary breach claim that a standard fidelity bond alone may not cover.

- The bond requirement applies even if the plan has never experienced fraud. ERISA’s bonding mandate is prophylactic — it exists regardless of a plan’s fraud history, size, industry, or the personal integrity of the individuals handling plan funds. Compliance is mandatory from the first day plan assets are handled.

- A plan sponsor can face personal liability if they authorize another person to handle plan funds without first ensuring that person is bonded. The responsibility is not limited to the individual doing the handling — anyone who authorizes another person to perform handling functions is also responsible for verifying that bonding is in place.

- The $500,000 bond cap does not mean $500,000 is the right amount for every large plan. For a plan with $10,000,000 in assets, the required bond is $500,000 — but if the same fiduciaries handle funds across multiple plans, each plan’s 10% requirement is calculated separately, and the total bond may need to exceed $500,000 to cover all plans adequately.

- ERISA was passed partly in response to a specific scandal. The Teamsters Central States Pension Fund, which by the early 1970s had been heavily looted through sweetheart loans to organized crime-connected real estate developers in Las Vegas, was one of the most prominent catalysts for ERISA’s passage in 1974. The bonding requirement was a direct legislative response to documented, large-scale theft from American workers’ pension funds.

Leave a Reply